Dividends Decoded: The Price Investors Pay for Chasing Income

This article is a warning to anyone who owns or is considering investing in a dividend-based mutual fund or ETF

Over the last 20 years, dividend-based mutual funds and ETFs have, on average, underperformed the market and failed to deliver value to investors.

In a financial landscape where high dividend yields are often seen as a safe haven, a closer look at 20 years of data reveals a starkly different reality. Despite the allure of steady income, dividend-based mutual funds and ETFs have consistently underperformed the broader market – raising tough questions about the true cost of chasing yield. I will explain the fees, market inefficiencies, and tax pitfalls that have left investors with less than they expected.

But the investment banks, mutual fund companies, ETF sponsors and index providers behind those products have done quite well. Those funds and ETFs commanded $953 billion of the $30+ trillion in assets as of the end of 2024, and investors are paying an average expense ratio of 0.73%, according to data from Morningstar Direct.

Dividend-based funds and ETFs include any product that selects stocks based on their dividends. That includes products that select for high dividends, dividends with a history of growth, dividend “aristocrats” (a subset of stocks with consistently growing dividends), and other criteria. These products employ both passive and active strategies.

The track record for dividend investing

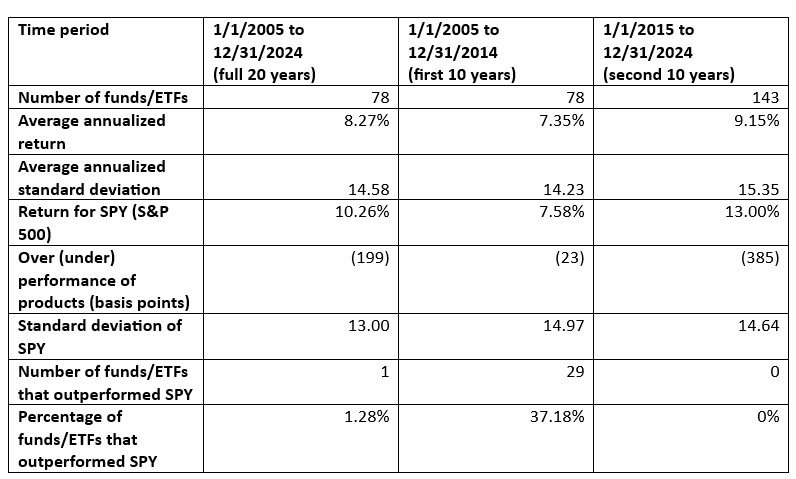

I looked at these products from the perspective of a long-term investor – someone who intends to hold them for 20 or more years in the accumulation or de-cumulation phase of retirement investing. According to Morningstar Direct, there are 248 U.S. funds and ETFs that its analysts classify as a dividend-based product. Of those, 143 have a 10-year history and 78 have a 20-year history, and those were the focus of my research.

The table below summarizes the performance of those funds on a pre-tax basis:

Dividend-based products underperformed the market (based on the ETF SPY) by 199 basis points over the last 20 years with slightly more risk (as measured by volatility or standard deviation). The degree of underperformance was greater in the more recent 10 years (385 basis points) than in the first 10 years (23 basis points).

Dividend-based investing has been riskier than the market and has produced lower returns.

Moreover, these results could be even bleaker if additional data – especially accounting for survivorship bias – were available. Morningstar uses analyst-based designations to assign funds and ETFs to its dividend-based category. Unfortunately, it does not have the number of dividend-based funds or ETFs retroactively to 10 or 20 years ago. Therefore, we don’t know the degree of survivorship bias in these returns (i.e., there were surely dividend-based funds and ETFs that existed 10 or 20 years ago but were terminated by their providers because of poor performance).

Only one product outperformed SPY for the full, 20-year period – the SIT Dividend Growth Fund (SDVGX). But that outperformance was in the first years (9.75% versus 7.58%) versus the second 10 years (10.91% versus 13.00%).

On an after-tax basis, the results were even worse. The funds and ETFs in this category have an average 30-day SEC dividend yield of 2.23% versus 1.27% for the S&P 500. Investors will pay a higher (ordinary income) tax rate on those excess dividends. This alone makes these funds undesirable for non-sheltered (taxable) accounts.

In August 2023, John Rekenthaler published an article about dividend investing. Rekenthaler’s results were more sanguine than mine, in part because he went back further in time to include the dot-com crash from 2000-2002. During that time, dividend stocks fared well, because most of the high-flying dot-com losers did not pay dividends. But don’t expect that phenomenon to repeat. Many of today’s technology-based market leaders now pay dividends (Apple, Microsoft, Nvidia, Meta and Alphabet). If you are looking for protection from a dot-com-like scenario, dividend stocks are not the way to do it.

During the last 10 years, ETF performance (9.35% average return) was slightly better than that of mutual funds (9.09%). There were only three ETFs with a 20-year performance history, so we cannot compare them to mutual funds for the full 20 years.

Persistence of returns

I looked at whether those funds and ETFs that performed best (in the top quintile) in the first 10 years went on to be in the top quintile in the second 10 years. Below are the results:

There was no persistence. If a fund or ETF was in the top quintile (top 20%) during the first 10 years, there was a higher likelihood that it would fall to the fifth (bottom) quintile than remain in the top quintile in the second 10 years.

Why did this happen?

The most obvious reason for this underperformance is the high fees (0.73% versus a few basis points for a cap-weighted index fund). It underscores the truism that it is incredibly difficult to outperform low-cost, highly diversified, cap-weighted index funds, and the probability of doing that goes down over longer time horizons.

From a market perspective, asset managers can make a powerful “pitch” to consumers that these products allow one to “live off the dividends” and not invade their principal to support their financial needs. This is a fallacy, since on a pre-tax basis, investors should be indifferent to whether their gains come from capital appreciation, dividends or coupons. On an after-tax basis, they should prefer capital gains. But the power of this marketing push has probably driven assets to these strategies, driving up prices and lowering future returns. The data suggests this is true, since the degree of underperformance was worse in the second 10 years than in the first (suggesting asset flows in the first 10 years). But it is nearly impossible to quantify this effect, so this is only a hypothesis.

All these products employ a degree of active management, since they deviate from the market-cap-weighted index. Virtually all academic studies have shown that active management underperforms an index fund over a long period of time.

Implications for advisors

Why isn’t there a fund or ETF that avoids dividends? It turns out that Alpha Architect filed for such a product in 2024, naming it the “anti-dividend ETF.” The idea was to avoid dividends by selling stocks before their ex-dividend period began. But the product was never launched.

The promise of “living off dividends” is more myth than reality. High fees, compounded by tax inefficiencies and a historical pattern of underperformance, demonstrate that investors will be better served by rethinking their approach. The evidence calls for a strategic shift – one that prioritizes long-term value over alluring, yet ultimately costly, income streams.

I invite you to explore these findings further and share your thoughts. For those interested in the detailed data behind this analysis, please feel free to contact me. Your feedback is invaluable as we continue to challenge conventional wisdom and search for more robust investment strategies.

Robert Huebscher was the founder of Advisor Perspectives and its CEO until the company was acquired by VettaFi in 2022. He was a vice chairman of VettaFi/TMX until April 2024.

Thank you, James.

Excellent analysis. Over the last twenty years, there’s been basically all downside to dividend funds. And the tax drag makes things a lot worse.

The idea of an anti-dividend fund is an interesting idea tho!